Your loan could be just a few steps away!

Bad Credit? We Could Help. Quick Approval Process

Get A Decision Online In Minutes With No Paperwork

Payday Loans in California

Payday loans in California are high-interest, short-term loans. Borrowers can get these emergency loans without collateral or credit score checks. Typically, they are supposed to be repaid on the user’s next “payday” in full.

Our California payday loans provide you the benefits of quick cash advances while also offering the lowest interest rates and longer repayment terms!

California Payday Loans: Laws & Regulations

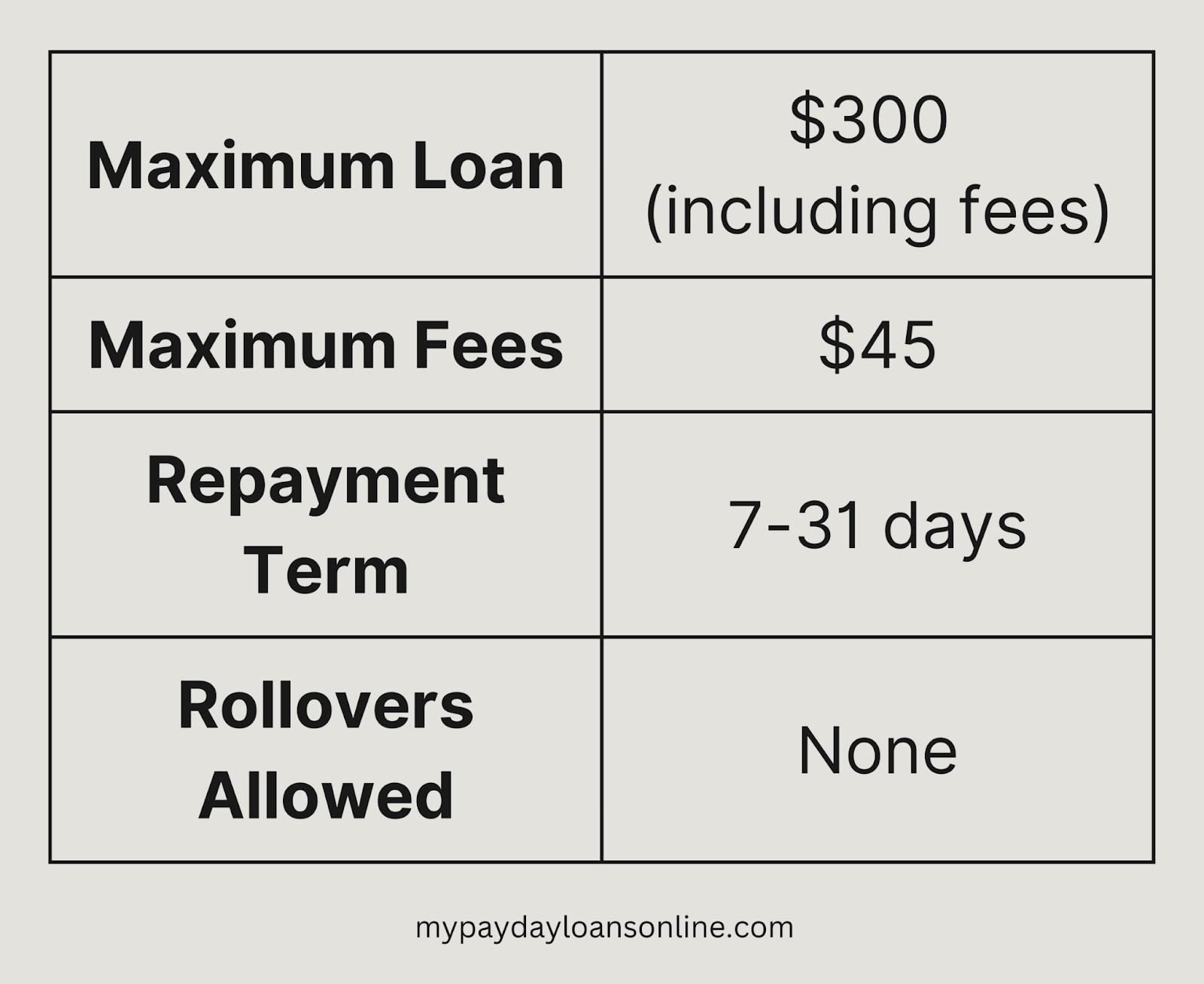

Considering the regulations, users can borrow up to $255 after writing a post-dated check of $300 to the lender. The fees charged cannot be more than 15 percent of the loan amount. There are additional resources offered by the DFPI to educate and safeguard residents in California against unfair lending practices.

My Payday Loans Online connects you with lenders who adhere to these regulations and provide you with only the best loan terms at lower interest rates (APR).

The APR for our California cash advance falls in the range of 5.99-35.99 percent. And, our repayment periods are between 61 days and 72 months.

How do I get the loan?

Our loan process is straightforward. Here’s how it works:

- You fill out the online payday loan application

- Our lender contacts you to explain the loan terms

- You confirm and proceed if it fits into your budget

- Receive, read carefully, and sign a soft copy of the loan agreement

- Funds are credited to your bank account on the same day

- You can later repay in monthly installments

What are the requirements to qualify?

We understand that emergencies don’t leave room for you to wait around for approval. That is why we have kept the documentation minimal for you.

Here’s what you need to be eligible for a payday loan in California:

- Age proof (you must be 18 years or older)

- Valid government-issued ID

- Steady income (pay stubs or bank statements)

- An active checking account

- Contact information

Tips for Borrowing Responsibly

We understand that the flexibility and accessibility of payday loans in California can result in making an uninformed choice. You can borrow mindfully by following these tips:

- Borrow only what you need to avoid unnecessary interest.

- Read loan terms carefully (APR, repayment period, fees).

- Repay on time to avoid late fees and extra costs.

- Ensure repayments fit your monthly budget.

- Compare lenders to get the best deal.

- Avoid multiple loans to prevent debt cycles.

- Set reminders for payment deadlines.

- Explore alternative loan options below.

- Build an emergency fund alongside loan payments.

Alternatives to Payday Loans in California

We offer you the best of both worlds – faster approvals like payday loans, and the option for monthly installments and longer time to repay, just like personal loans.

If you’re confused about whether to take a payday loan or not, there are other alternatives you may consider.

- Borrow from friends or family members.

- Talk to your employer for a salary advance if possible

- Take out credit card cash advances (if your card charges low APR)

- Opt for a secured loan to get lower interest rates

Why choose us?

There are a few features that make our cash advances one of the best online payday loans in California. This is why you can trust us:

- Lowest interest rates

- Repayment in monthly installments

- No credit score checks

- Faster approvals

- Minimal documentation

- Longer repayment period

- Encrypted website to secure your data

- Transparency in loan terms

For more information on payday loans in California, you can reach us at the contact information we’ve provided.